Ready Reckoner for Financial Frauds

Sougata Saha (Cyber Forensic Enthusiast, Ex-NFSU Student, Masters in Cyber Forensics)

May 27, 2026

In

recent years, India has witnessed an alarming surge in cybercrimes,

particularly financial frauds, driven by rapid digitalization, widespread

adoption of UPI, internet banking, and mobile payments. According to Ministry

of Home Affairs (MHA) data, cybercrime cases rose by 24% in 2025, reaching 28.15

lakh reported incidents compared to 22.68 lakh in 2024. Indians lost

approximately ₹22,495 crore

to these frauds in 2025, with investment scams accounting for over 75% of the

total losses. Common tactics include fake investment apps, UPI spoofing,

digital arrest scams, phishing calls impersonating banks or police, and KYC

frauds.

This

trend reflects the double-edged sword of India’s digital growth. While UPI

transactions have skyrocketed, so have sophisticated social engineering attacks

targeting both urban and rural populations. Even though government initiatives

like the National Cyber Crime Reporting Portal, 1930 helpline, and coordination

between RBI, NPCI, and banks have helped in faster fund blocking and some

recoveries, the sheer volume of cases highlights a growing challenge.

Closer

to home in Tripura, the situation mirrors the national crisis but with

its own regional intensity. The following table shows a brief scenario about

the data of financial fraud in Tripura -

|

Financial

Year

|

Cyber

Crime Complaints Registered

|

Amount

Lost to Cyber/Financial Fraud (₹

Crore)

|

Source

Notes

|

|

2023-24

|

2,255

|

>12.39

|

Tripura

Legislative Assembly data (March 2026 release)

|

|

2024-25

|

3,304

|

~25.73

|

Tripura

Legislative Assembly data

|

|

2025-26

(up to ~March 2026)

|

3,336

|

~38.09

|

Tripura

Legislative Assembly data (partial year)

|

|

Cumulative

(since 2021, as of Aug 2025)

|

-

(269 victims)

|

51.49

(Rs. 33.84 lakh recovered)

|

Tripura

Police DGP briefing (official)

|

Cyber

fraud, especially online cheating and phishing, has increased significantly,

affecting common citizens, students, and senior citizens alike. Northeast

states like Tripura, with improving digital connectivity but varying levels of

cyber awareness, are becoming soft targets for pan-India scam networks often

operated from outside the region.

Financial

fraud is not just a law enforcement problem - it is a shared responsibility.

While agencies like the Indian Cyber Crime Coordination Centre (I4C), State Cyber

Cells, Police, RBI, and NPCI continue to strengthen reporting mechanisms, fund

tracing, and preventive tools, common citizens play an equally critical role.

Awareness, vigilance, and prompt action by individuals can prevent most scams

and improve recovery rates dramatically.

By

educating ourselves and our families, following strict safety protocols,

reporting incidents immediately, and staying updated on emerging threats, we

can collectively reduce the impact of these crimes. This guide is designed to

empower you with actionable Do’s and Don’ts — from the first critical minutes

after a fraud to long-term prevention strategies.

Remember:

Staying safe in the digital world is a continuous habit, not a one-time effort.

Let us build a more aware and resilient Tripura and India together.

Listed here are some majors that

should be followed when any financial fraud takes place -

Phase

1: Immediate Actions (First 30–60 Minutes – Most Critical)

Do’s:

- Stop All Transactions

& Freeze Accounts

- Call your bank’s 24×7

customer care immediately (numbers are on the back of your card or

bank app).

- SBI: 1800-11-2211 /

1800-425-3800

- PNB: 1800 1800 / 1800

2021

- HDFC: 1800-202-6161

- ICICI: 1800-108-0123

- Axis: 1860-419-5555

- Clearly say: “My

account has been fraudulently transacted. Please block my account,

debit/credit card, and UPI instantly.”

- Ask for a Fraud

Reference Number from the bank.

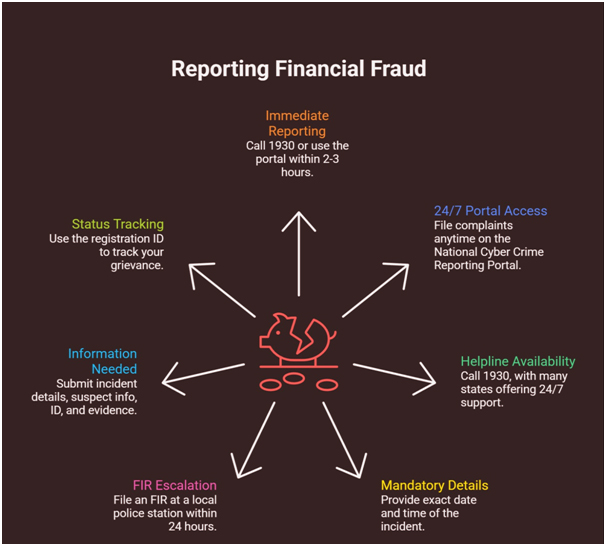

- Report on National

Portal

- Go to https://cybercrime.gov.in

[Available 24*7].

- Click “Report Other

Cyber Crime” → Choose “Financial Fraud”.

- Fill details

carefully: amount, date, time, scammer’s number/UPI ID, how the fraud

happened.

- Upload all screenshots

and evidence.

- You will get an Acknowledgement

Number (save it).

- Call 1930

- Dial 1930

(National Cyber Crime Helpline) [Available from 09:00 AM – 06:00 PM].

- Tell them you want to

report financial fraud. They will guide you and may escalate to the

concerned state cyber cell.

Don’ts:

- Do not wait till morning or

“see if money comes back”.

- Do not try to transfer money

to “safe accounts” suggested by anyone.

Image – Detailled Flowchart of

Reporting incident to National Cyber Crime Reporting Portal

Phase

2: Next 2–24 Hours

Do’s:

- File FIR

- Visit your local

police station and file an FIR.

- Alternatively, many

states allow online FIR for cybercrime.

- During Visit to Local

PS and filing FIR show the acknowledgement received from Cybercrime

Reporting Portal.

- Carry printed

screenshots and cybercrime.gov.in acknowledgement.

- Secure All Digital

Accounts

- Change passwords for:

- Email (Gmail/Outlook)

- All banking apps

- UPI apps (PhonePe,

Google Pay, Paytm, BHIM)

- Aadhaar, PAN,

DigiLocker

- Enable 2-Factor

Authentication (2FA) or biometric login.

- Check “Linked Devices”

and log out from unknown devices.

- Scan for Malware

- Use trusted apps like

Malwarebytes, Quick Heal, or Google Play Protect.

- Avoid using the same

phone for banking until scanned.

- Preserve Evidence

Properly

- Save everything in a

separate folder:

- Transaction SMS

- Call logs

- WhatsApp/SMS chats

- Bank statement

- UPI transaction ID

- Take photos of

everything with date & time visible.

Don’ts:

- Do not delete any message or

call record.

- Do not click any link sent

by the scammer or “helper”.

Phase

3: Follow-up & Recovery (Next 1–30 Days)

Do’s:

- Track Your Complaint

- Log into

cybercrime.gov.in regularly using your acknowledgement number.

- You can also track via

the Citizen Portal of your state cyber cell (e.g., Delhi,

Maharashtra, Karnataka have dedicated portals).

- Coordinate with Bank

- Share your cybercrime

complaint number with the bank’s fraud team.

- Banks work with NPCI

(for UPI) and RBI for fund tracing.

- Credit Freeze (if

needed)

- If large amount is

involved or identity theft suspected, contact CIBIL/Experian/Equifax to

place a fraud alert.

- Seek Legal Help (if

amount is high)

- Contact a cyber law

expert or approach consumer court / cyber cell senior officer.

Don’ts:

- Do not pay any “recovery

agent”, “ethical hacker”, or person claiming to be from “Cyber Crime

Department” who asks for money.

- Do not share your OTP,

Aadhaar, or bank details with anyone claiming to help.

Common

Recovery Timelines in India

- 0–2 hours:

Highest chance (70–90% in some UPI cases)

- 2–48 hours:

Moderate chance if money is still in mule account

- After 7 days:

Recovery becomes difficult but still possible if traced

- Many cases take 30–90 days

for full investigation

Most

Common Financial Frauds in India Right Now

- UPI QR code / number spoofing

- Fake customer care calls

- Fake investment apps (trading,

crypto, gold)

- Digital Arrest / impersonating

police

- KYC update / SIM swap fraud

- Loan app harassment

Prevention

Tips (Must Follow After Recovery)

- Never share OTP

- Verify every call by calling

official bank number yourself

- Use virtual UPI IDs instead of

phone number

- Avoid public Wi-Fi for banking

- Keep transaction limit low on UPI

- Install apps only from Play Store /

App Store

How

to Stay Safe from Financial Fraud – From Your End

Prevention

is always better than cure. Here’s a detailed, practical checklist you

can follow daily to protect yourself from UPI scams, phishing, fake calls,

investment frauds, and other common financial cybercrimes.

1.

Golden Rules – Never Break These

- Never share

your UPI PIN, OTP, password, CVV, or Aadhaar details with anyone —

not even if they claim to be from bank, police, or tech support.

- You enter UPI PIN only to send

money, never to “receive money”, “verify account”, or “update KYC”.

- Banks/RBI/NPCI never ask for

sensitive info over phone, WhatsApp, or email.

- If someone asks for your PIN/OTP →

It’s a scam. Hang up and verify directly.

2.

UPI & Banking App Safety (Most Important in India)

- Set low transaction limits

in your UPI apps (e.g., ₹5,000–10,000 per day for new contacts).

Increase only when needed.

- Use UPI Lite or wallets for

small daily payments (less risk to main bank account).

- Always verify the receiver’s

name that appears before confirming payment.

- Be extremely careful with “Collect

Request” or payment links sent by others.

- Never scan QR codes received via WhatsApp/SMS

for “receiving money” — scammers use fake ones.

- Enable transaction alerts (SMS +

app push notifications) and check them immediately.

New

RBI/NPCI Rules (2026): Many banks now have extra

verification or cooling periods for high-value or first-time large transfers.

Use this delay wisely if something feels off.

3.

Device & App Security

- Download only official apps

from Google Play Store or Apple App Store (check developer name: Google

Pay by Google, PhonePe, etc.).

- Keep your phone, apps, and OS updated

always.

- Use strong screen lock (biometric +

PIN).

- Install reputable antivirus (e.g.,

Google Play Protect, Malwarebytes).

- Avoid public Wi-Fi for banking. Use

mobile data or trusted networks.

- Never install screen-sharing apps

(TeamViewer, AnyDesk) at anyone’s request.

- Do not root/jailbreak your phone.

4.

Password & Authentication Best Practices

- Use strong, unique passwords (mix

of letters, numbers, symbols).

- Enable 2-Factor Authentication

(2FA) or biometric login everywhere.

- From 2026, many digital transactions

require mandatory two-factor authentication.

- Avoid saving passwords/card details

in browsers.

- Change passwords periodically and

after any suspected issue.

5.

Daily Habits to Avoid Scams

- Ignore unknown

calls/SMS/WhatsApp claiming issues with

your bank, KYC, PAN, Aadhaar, or promising rewards/jobs/investments.

- Verify by calling the official bank

number yourself (from bank website or passbook).

- Use Truecaller or similar to

identify suspicious numbers.

- Think twice before clicking any

link — type the official website/app directly.

- For investments: Only use

SEBI-registered platforms. High returns with “guaranteed” profit = red

flag.

- Avoid clicking “Update KYC” or

“Account Blocked” links sent unsolicited.

6.

Account Monitoring

- Check your bank statements and UPI

history regularly (at least weekly).

- Set up email/SMS alerts for every

transaction.

- If you see an unknown transaction →

Immediately block cards/UPI and report.

- Review linked devices and log out

from unknown ones.

7.

Extra Layers of Protection

- Use virtual UPI IDs (not

directly your phone number) where possible.

- Freeze UPI when not in use (option

available in many apps).

- For large amounts, use NEFT/RTGS

with extra verification instead of UPI.

- Keep a separate low-balance account

for daily UPI use.

- Educate family members (especially

elderly) about these rules.

Quick

Red Flags to Watch

- Urgency (“Act now or account will

be blocked”)

- Too-good-to-be-true offers

- Requests for remote access or

screen sharing

- Fake customer care numbers

- Unsolicited “refund” or “prize”

messages.

Pro

Tip: Pause for 30–60 seconds before approving

any payment. Scammers rely on panic and quick decisions.

Follow

these habits consistently, and your risk of falling for financial fraud drops

dramatically. Most scams succeed because people trust the wrong person or act

in a hurry.

(Tripurainfo)

more articles...